Debt Programs

Many of San Francisco's capital improvements are funded with voter-approved General Obligation Bonds (G.O. Bonds), General Fund debt called Certificates of Participation (COPs), or revenue bonds.

Issuing debt is a typical method for financing capital enhancements with long useful lives and high upfront costs, which the City would not be able to cover through the Pay-Go Program. The use of debt also spreads the financial burden of paying for facilities between current residents and future generations who will also benefit from the projects. In the context of the COVID-19 pandemic, it is important to acknowledge the meaningful role that debt can play in San Francisco’s economic recovery, as documented in the Economic Recovery Task Force Report (see summary in Building our Future chapter). More so than in past Capital Plans, the debt programs are programmed with an eye towards local economic stimulus and building a more resilient, equitable San Francisco as part of the City’s recovery from the pandemic.

Health and Recovery Bond 2020

In November 2020, voters approved the Health and Recovery Bond, a multi-service area bond that will address some of San Francisco’s most urgent needs: addressing the twin challenges of mental health and homelessness; and investing in large, shovel-ready parks and street infrastructure projects that will serve as an engine for growth and create local jobs that will help jumpstart San Francisco’s economy. This $487.5 million bond provides $207 million to invest in permanent supportive housing, shelters and facilities that deliver services to people struggling with mental health and substance use disorders; $239 million for capital needs in the City’s park system, including citywide parks like Golden Gate Park, Lake Merced, and McLaren Park, neighborhood parks like Buchanan Mall, Gene Friend Recreation Center, Herz Playground, and India Basin, community gardens, and trails; $41.5 million to address public right of way and public spaces, including street resurfacing, ADA curb ramp construction and maintenance, and repair and maintenance of street structures like the Third Street Bridge and Filbert Street Steps.

General Obligation Bonds

G.O. Bonds are backed by the City’s property tax revenue and are repaid directly out of property taxes through a fund held by the Treasurer’s Office.

The Plan structures the G.O. Bond schedule around the notion of rotating bond programs across areas of capital need, although the City’s debt capacity, election schedules, and capital needs also inform these levels. This approach was established in the original Capital Plan and has been maintained ever since.

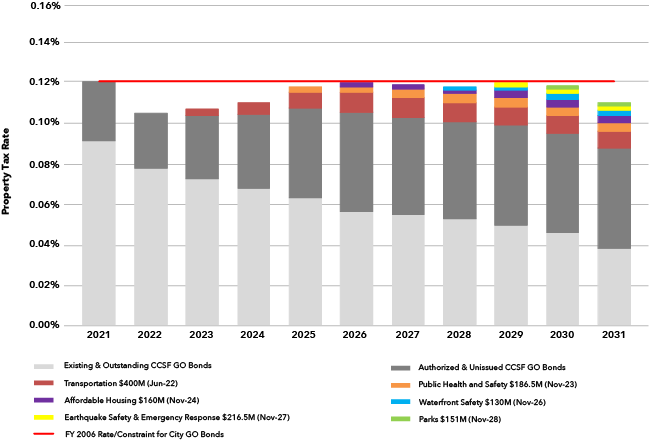

Priority areas of need for capital improvements include Earthquake Safety & Emergency Response, Parks & Open Space, Transportation, Public Health, and the Waterfront. As part of incorporating Affordable Housing into the Capital Plan, there is also the first advance-planned bond in that area. The Plan occasionally recommends bonds outside these categories if there is a demonstrated capital need that the City would otherwise not be able to afford. Table 5.1 lays out the planned G.O. Bond schedule for upcoming elections.

Chart 5.1 illustrates the impact on the local tax rate of issued, expected, and planned G.O. Bond debt. The red line represents the property tax limit policy established in 2006 that sets the annual level of bond debt repayment. The space between the red line and the bars on the chart illustrates the projected capacity for bond debt for each year. All amounts attributed to future bonds are estimates and may need to be adjusted to account for new federal and state laws, programmatic changes, site acquisition, alternate delivery methods, changing rates of construction cost escalation, and/or newly emerged City needs.

The G.O. Bond program’s capacity is largely driven by changes in assessed value and associated property tax revenues within the city. The recent economic boom increased assessed value growth over the past several years, but that growth is expected to slow now due to the COVID-19 crisis. While the passage of recent bonds is a sign of the effectiveness of the capital planning process, it also impacts the available bond capacity going forward. The passage of three large bonds totaling $1.7 billion since 2019 means there is considerably less capacity for this 10-year capital planning cycle compared to previous ones. For more information on the G.O. Bond policies and past bonds, please see the Introduction chapter.

In addition to this program, external agencies may also issue G.O. Bonds. For example, City College passed a $845 million bond in FY2020, and SFUSD has plans for a $1 billion bond on the November 2022 ballot.

Table 5.1

| G.O. Bond Program | ||

| (Dollars in Millions) | ||

| Election Date | Bond Program | Amount |

| Jun-22 | Transportation | 400 |

| Nov-23 | Public Health | 187 |

| Nov-24 | Affordable Housing | 160 |

| Nov-26 | Waterfront Safety | 130 |

| Nov-27 | Earthquake Safety & Emergency Response | 217 |

| Nov-28 | Parks and Open Space | 151 |

| Nov-31 | Public Health | TBD |

| Total | 1,245 | |

Chart 5.1

Certificates of Participation

Certificates of Participation (COPs) are backed by a physical asset in the City’s capital portfolio and supported through annual General Fund appropriations or revenue that would otherwise flow to the General Fund. The City utilizes COPs to leverage the General Fund to finance capital projects and acquisitions. Funding from COPs is planned to support basic City responsibilities such as relocating City staff from seismically deficient buildings.

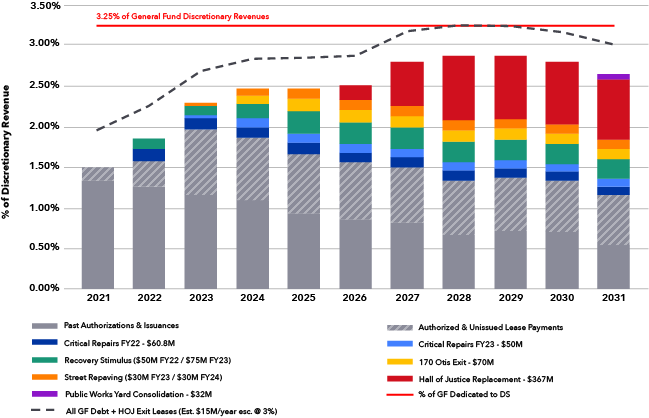

Table 5.2 shows the Capital Plan’s COP Program for the next ten years. This Program includes two years of issuances for critical repairs totaling $111 million, as well as two years of issuances for street resurfacing totaling $60 million. Together, these four issuances help mitigate cuts to the Pay-Go Program due to the recession. In addition, this program also includes two years of issuances for recovery stimulus totaling $125 million. These issuances will support projects that serve as local economic stimulus and help build a more resilient and equitable San Francisco as part of the city’s recovery from the COVID-19 pandemic. Chart 5.2 shows the planned COP Program against the policy constraint for General Fund debt not to exceed 3.25% of General Fund Discretionary Revenue, represented by the red horizontal line. The black line depicts the annual lease costs related to the Hall of Justice Administrative Exit efforts approved in 2018, which are also counted against this Program’s constraint.

The bottom portions of the columns represent debt service commitments for previously issued and authorized but unissued COPs, including the debt issued for the Moscone Center, the War Memorial Veterans Building, and the Animal Care & Control Shelter replacement. New obligations are represented in discrete colors, beginning in FY2022. As with the G.O. Bond Program, all amounts attributed to future COP-funded programs are estimates and may need to be adjusted in future plans to account for new federal and state laws, programmatic changes, site acquisition, alternate delivery methods, changing rates of construction cost escalation, and/or newly emerged

City needs.

Table 5.2

| COP Program | ||

| (Dollars in Millions) | ||

| Fiscal Year of Issuance | Project | Amount |

| FY2022 | Critical Repairs | 61 |

| FY2022 | Recovery Stimulus | 50 |

| FY2023 | Relocation of HSA Headquarters | 70 |

| FY2023 | Critical Repairs | 50 |

| FY2023 | Recovery Stimulus | 75 |

| FY2023 | Street Resurfacing | 30 |

| FY2024 | Street Resurfacing | 30 |

| FY2025 | HOJ Consolidation Project | 367 |

| FY2031 | Public Works Yard Consolidation | 32 |

| Total | 765 | |

Chart 5.2

Revenue Bonds

Revenue bonds are a type of debt that is repaid from department or other revenue streams. Revenue bonds are typically used by the City’s enterprise departments (SFMTA, Port, SFPUC, and SFO), which generate their own revenues from fees paid by users of services provided by those agencies. This type of debt is repaid solely by users of those projects and therefore does not require payments from the General Fund. Examples of projects funded by revenue bonds are the SFPUC’s Water Systems Improvement Program and the Airport’s Terminal Renovation Program.

Table 5.3 shows the currently planned amount of revenue bonds to be issued over the 10-year term of this Plan.

All revenue bond issuances are subject to change based on market conditions and cash flow needs of the associated projects.

Table 5.3

| Planned Revenue Bond Issuances FY2022-31 | |||

| (Dollars in Millions) | |||

| Agency | FY22-26 | FY27-31 | Total |

| SFPUC | 4,549 | 2,236 | 6,785 |

| Airport | 1,189 | 0 | 1,189 |

| Total | 5,738 | 2,236 | 7,974 |